Can I convert a level term or decreasing term policy to a whole life policy?

Many term life policies include ‘riders’ which allow you to convert them to whole life policies. If this is something you might want to consider you should make sure the term life policy you intend to buy offers this.

How long do level term and decreasing term policies last?

It depends on what you’re looking for and what an insurer offers. Most level and decreasing term policies are taken out for between 25 and 40 years, but it may be possible to get longer ones, depending on your age at the start of the policy.

Do I have to have decreasing term life insurance with a mortgage?

There’s no general obligation, legal or otherwise, to take out decreasing term life insurance when you take out a mortgage. However, some lenders may make it a binding term of the mortgage contract that you have some form of life insurance in place to cover the cost of repaying the loan.

Can I cash in a level term or decreasing term policy?

No, unlike whole life policies, fixed term life policies don’t build up any cash value. Their only function is to pay your beneficiaries should you pass away while the policy is in force.

Term life and whole life insurance

Term life and whole life policies are fundamentally different. Whole life policies have no fixed end date and continue in place until the insured passes away, whenever that may be. Term life insurance policies have an expiry date that’s fixed from the start. If the insured is still living when the policy reaches that date, their cover comes to an end.

What is level term life insurance?

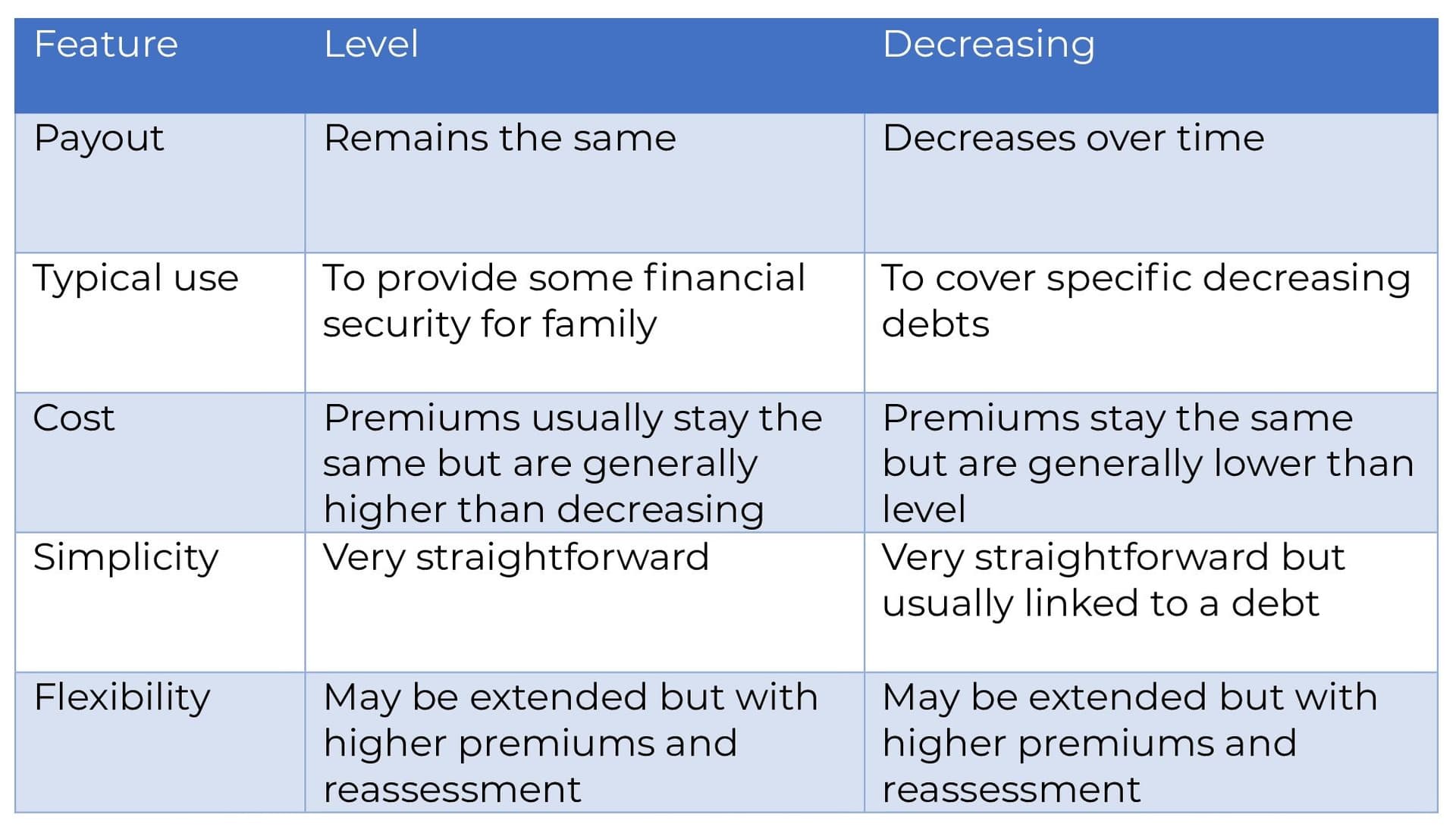

This type of policy is taken out to insure the life of the policyholder, or in some circumstances a third party, for a fixed number of years. What makes it ‘level’ is that the sum payable on the death of the insured is set when the policy is taken out and remains the same for the duration.

So how does level term life insurance work? Level term policies can last for anything from 5 to 40 years, although depending on the age of the insured at the start of the policy it may be possible to exceed 40 years. The monthly premiums often stay the same throughout the life of the policy, but it’s not uncommon for them to be reviewed upwards as the insured grows older and possibly experiences a decline in health. If the premiums do increase, the sum insured will not. The rising cost is merely a consequence of the increasing risk.

What is decreasing term life insurance?

As its name suggests, decreasing term life insurance runs for a fixed period and the sum insured is reduced over the life of the policy. At the end of the fixed term the cover ends. Although the payout decreases, the premiums usually stay the same throughout, but they also tend to be lower than for some other types of term policy. This is because the risk to the insurer decreases over time, making it less expensive for them to provide cover.

Purpose

Level term policies are typically chosen by people who want to combine the certainty of future financial security for their families with consistent, affordable premiums. They can work well for people who only feel the need to support their loved ones for a finite period – perhaps until their children have grown up and established themselves in the adult world.

Decreasing term policies are mostly chosen by people who have some form of long-term debt, as a means of ensuring it’s repaid should they pass away. It’s particularly suitable for mortgages, where the sum owed to the lender decreases over the years until it’s paid off. A decreasing term life policy can be arranged to run concurrently with the mortgage so that, if the insured should die at any point, there will be sufficient funds from the policy to pay off what remains of the mortgage debt. Once the policy reaches its fixed expiry date, cover will end.

Cost

The premiums for level term policies usually remain the same although, as already mentioned, the insurer may have the right to increase premiums if the insured’s health deteriorates significantly. The premiums for decreasing term policies also remain the same but they are calculated at a lower level because of the diminishing risk to the insurer.

Simplicity

Both level and decreasing policies are relatively simple and straightforward. The final payout, whether fixed or decreasing, is calculated at the start so you know what you’re getting. In most cases the premiums won’t change so you have certainty throughout. Where it can become more complicated is if your circumstances change and you wish to extend either. If your insurer agrees to your request, they’re likely to increase your premiums and you may also have to undergo some form of additional underwriting to reassess the new level of risk.

Disadvantages

The main drawback with level term insurance is that it can’t keep pace with inflation. Over a period of several years the true value of the fixed payout will be eroded, even if the inflation rate remains low as it did from 2012 until 2021. Let’s as an example a sum insured of £200,000 taken out in 1999. Using the Bank of England’s , that sum should now be over £370,000. If the policy paid out today it would have lost 46% of its value.

Is level term or decreasing life insurance better?

As you can see, it’s a little like trying to compare apples and bananas. The real question is, what do you need your life insurance for? Decreasing term may be ideal for the needs of one person and completely unsuitable for those of someone else.

Switching from one to the other

If your circumstances change during the life of your policy, you may find that it no longer fulfils its purpose and you’d like to convert your cover into the other kind. This is not usually a case of simply switching from level to decreasing or vice versa. More likely it will involve taking out a new policy, which will mean a fresh application and underwriting process. Once you’ve got your new policy you can cancel the old one but turning your existing policy into a different one isn’t really an option. It may be a good idea to take professional advice.

Can you have both level and decreasing term life insurance?

You can have as many life insurance policies as you like and there’s no reason not to have both level and decreasing simultaneously, although the cost of two will naturally be greater than one. There are two ways of doing this.

Hybrid policies

Some insurers offer policies that combine elements of both. You would take out a policy which essentially provides two strands of cover – level and decreasing – usually paid for with a single premium. There may be cost-efficiencies in arranging this with a single insurer, which would keep it simple.

Separate policies

Alternatively, you can take out separate policies, either with one insurer for both or different insurers for each. This is likely to give you more opportunities to customise the policies so they will more closely meet your needs, although it may be more expensive than the hybrid option.

Switching from one to the other

If your circumstances change during the life of your policy, you may find that it no longer fulfils its purpose and you’d like to convert your cover into the other kind. This is not usually a case of simply switching from level to decreasing or vice versa. More likely it will involve taking out a new policy, which will mean a fresh application and underwriting process. Once you’ve got your new policy you can cancel the old one but turning your existing policy into a different one isn’t really an option.

Is level term or decreasing life insurance better?

As you can see, it’s a little like trying to compare apples and bananas. The real question is, what do you need your life insurance for? Decreasing term may be ideal for one person’s needs and completely unsuitable for another’s.

Life insurance for young adults doesn't have to be complicated or costly. This comprehensive guide covers why purchasing life insurance as a young adult locks in lower rates based on current health and how to pick the proper policy length and provider for your situation.

Introducing Theea's Coverage Calculator: the intuitive insurance tool inspired by thousands of customer conversations that turns anxiety into tailored advice and confusion into confident choices.

With decreasing term life insurance, the main drawback is built into its design – it may adequately cover a debt such as a mortgage but it’s unlikely to provide any extra funds for your family’s other costs.

We’re expanding our perks with two new additions designed to turn good intentions into healthy habits. Discover everything you can get for free with an Eleos policy.